In 2022, stock and bond investors have been pummeled, losing money in both asset classes for three consecutive quarters, a first in at least 45 years. In previous letters, we have discussed our defensive stance...

![]()

Rope-a-Dope1

In 2022, stock and bond investors have been pummeled, losing money in both asset classes for three consecutive quarters, a first in at least 45 years.2 In previous letters, we have discussed our defensive stance, holding “dry powder”3 and remaining disciplined. Yet, as openings occur, we take our shots. We continue to find “money-good”4 bonds and leveraged loans that have attractive yields with potential for additional upside if anticipated events come to pass:

- long-term debt reclassifying to current liabilities

- event-driven corporate actions

- Mergers and acquisitions

- De-leveraging initiatives

- Relief from debt covenant constraints

- potential future takeover targets

Below, we discuss some of the indicators that we are watching closely and describe some of the opportunities we are seeing that should allow us to “punch above our weight.”

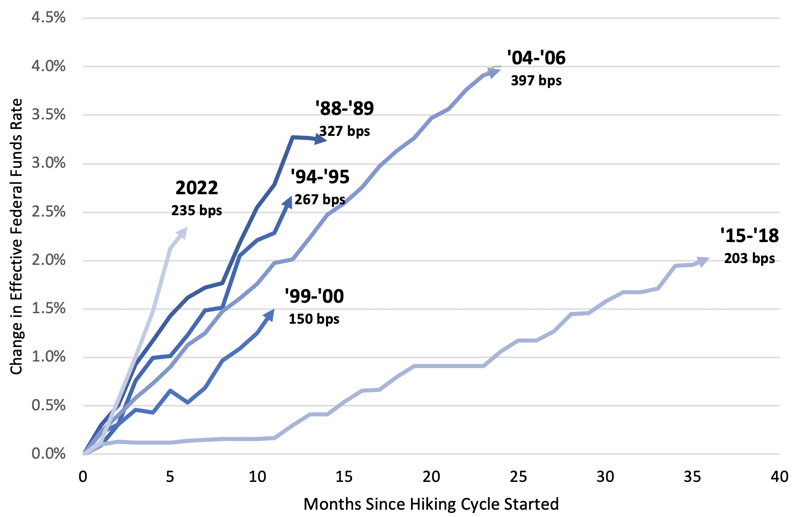

Rapid Rise in Interest Rates

Comparison of Speed of U.S. Interest Rate Hikes5

As the Fed grapples with inflation, which is no longer “transitory,” the financial markets have sold off sharply in response to the most rapid interest rate hikes in recent history. In 2022, the Fed Funds rate rose by 235 basis points in six months with indications that this will continue. The financial markets fear, but may not have fully priced in, the possibility that, ultimately, the Fed’s actions or the geopolitical backdrop will cause something to break.6 With the dramatic rise in rates, we believe the economy will slow, corporate profit margins will shrink, working capital costs will increase and debt service will be more expensive. These factors are concerning, but, more importantly, also create opportunities that may be exploited if patience and diligence are exercised.

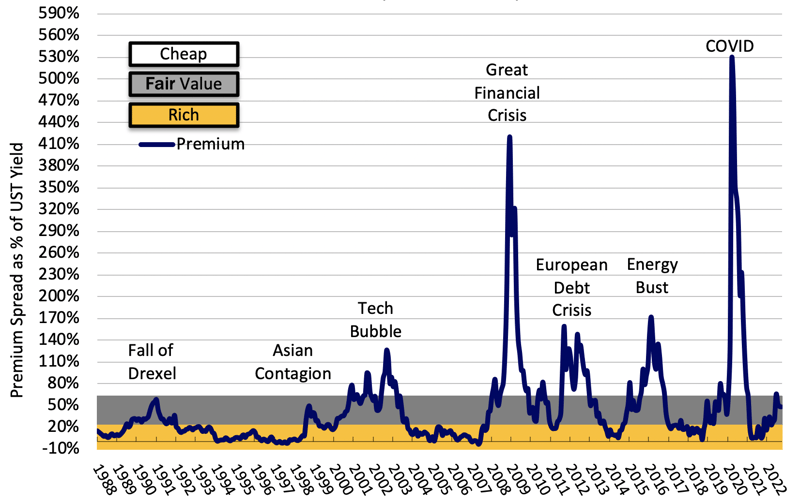

HY Spreads versus Risk Free Rate

Risk Adjusted, After Tax-Premium Spread of High Yield over 10-Year UST

(1988 - Current)7

Credit spreads in the high yield market are almost “cheap” as they have widened by approximately 220 basis points to 550 basis points8 since the end of 2021. This is slightly below the 25-year average of 552 basis points,9 leaving room to go wider if unforeseen economic or political events hit the market with a haymaker.10 However, as noted in our 2Q22 letter, a high yield investor who avoided the value destruction in telecom and utility bonds in 2002, a negative year for high yield overall, would have had a positive return for the year. Similarly, an investor avoiding the deterioration in energy credits in 2015-16 would have experienced far better performance. Looking forward, we are avoiding industries that continue to struggle due to the impact of COVID, such as cruise lines and movie theaters, and those that will be most impacted by rising costs or cyclical risks to demand, including building materials, chemicals and auto parts. The sharp rise in interest rates and the widely expected resultant recession may also be the “zombie killer”11 that finally forces a wave of restructurings among companies reliant on accommodative capital markets to provide cash infusions to cover interest expense. That said, as a result of the dislocation that has already occurred, there are a lot of quality companies with “money good” debt yielding 7.5-11.5% with maturities in the 1-3-year sweet spot.

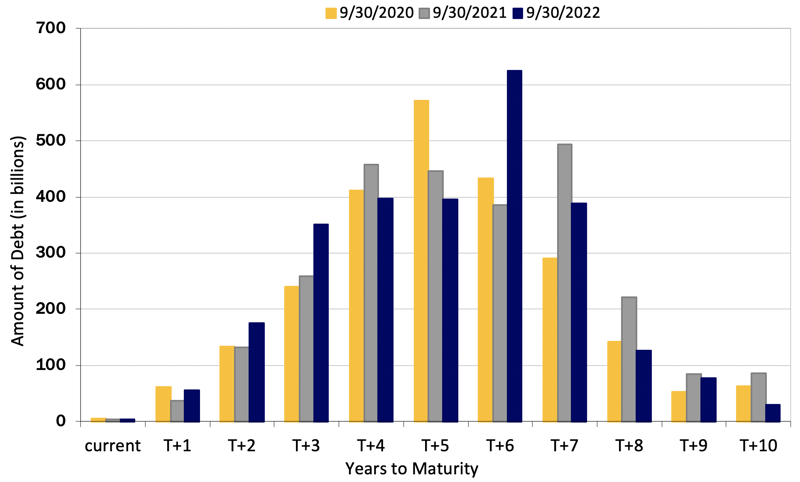

Wall-of-Worry Not So Worrisome

Maturities Moving Out - HY Loans and Bonds12

The rise in rates should have a more muted impact on the high yield market than in previous rate-hike cycles as many borrowers took advantage of the low rates that prevailed in 2020 and 2021 to reduce their borrowing cost and extend maturities. As shown above, in 3Q20, a large portion of the corporate credit market was likely to be faced with the need to refinance debt obligations in the 2024-25 period (i.e. orange bars in T+4 and T+5). With the new-issuance market very active despite the pandemic, debt coming due in that period has now been reduced significantly (i.e. blue bars in T+2 and T+3) while the bulge in upcoming maturities has been pushed out to 2028 (i.e. blue bar in T+6). Thus, a large portion of high yield issuers completed financings giving them low locked-in borrowing costs for several years. Similarly, many homeowners have benefitted from low interest rate mortgages. Hence the long-awaited distress cycle may be put off a little longer.

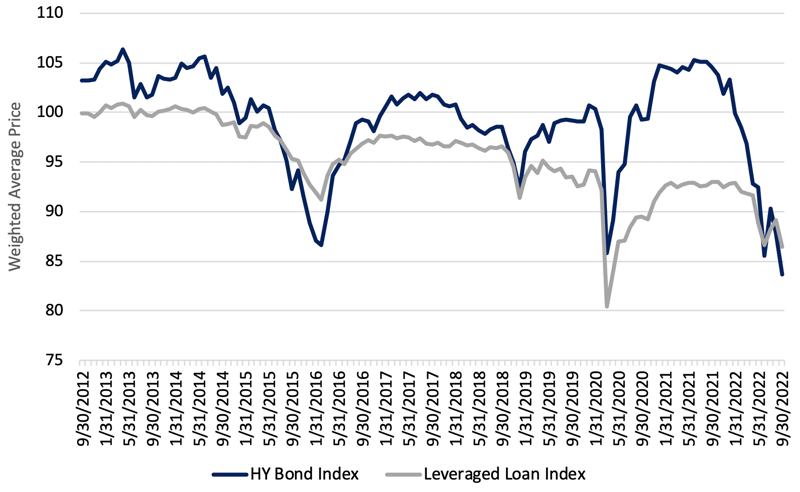

Bonds and Loans Trading at a Discount

ICE BofA HY Index Par Weighted Price vs

S&P/LSTA U.S. Leveraged Loan Select Equal Par Value Index13

When interest rates go up, bond prices go down. Consequently, corporate debt is now trading at a discount. The current year has been unusual in that the average bond in the ICE BofA High Yield Index has experienced a price decline of nearly 20 points since the end of 2021 as interest rates have moved up and credit spreads have widened. Such a sharp decline would not be unusual for distressed bonds but, in the absence of a sharp deterioration in credit quality, it is highly unusual. These discounts create the opportunity for an investor to achieve a return in excess of today’s yield to maturity should a corporate event cause a credit quality upgrade or repayment prior to maturity. Loans are also trading at a discount, but because their interest rates are floating, they have not experienced as much price deterioration as fixed rate bonds. Still, loans trading at a discount may also provide us with opportunities resulting from corporate events.

Where we are taking our shots

While we remain defensive, we are finding opportunities to throw a few “jabs” and “uppercuts” when we see openings. These investments fall into four categories, but in general are premised on events we expect to take place within a relatively short time frame.

Called Bonds and SPACs – Bonds that have been called and are expected to be repaid via refinancing or cash on hand at the end of the call period, typically 30-90 days out. Refinancing among high yield bonds has diminished as the cost of new financing has increased dramatically. However there continues to be a steady flow of investment grade calls and tenders as the “treasury make-whole” call protection,14 which historically resulted in prohibitively expensive call premiums for these bonds, has now fallen to zero. Thus, the market yield to exit for investment grade bonds has gravitated to about 4.00-5.00%for calls expected to be completed in 2-6 weeks. Meanwhile, the market for the few high yield bonds that are being called has risen to about 4.50-5.50%. This compares to the 2.00% yield to exit that was typical for called high yield bonds as recently as the end of 2021. Similarly, the effective yield on SPACs with liquidation dates up to 9 months has risen to 5.5-6.00%.

Long-term Debt Reclassifying to Current Liabilities – Bonds and loans with maturities 1-2 years out. Once the maturity of these obligations falls within one year, they must be shown on the issuer’s balance sheet as current liabilities, and their auditors must opine on their ability to pay them when they are due. Typically, borrowers prefer to repay or refinance their debt when there is at least one year to maturity to avoid this issue.

GoDaddy (GDDY) - GoDaddy is the “800-pound gorilla” in the web hosting space as its attractive domain pricing and breadth of services has helped make it one of the largest global domain registrars. During the first half of 2022 the company has continued to display operating strength with revenues up over 10% and normalized EBITDA up nearly 25%. Meanwhile they continue to produce significant free cash flow, with over $450mm generated year-to-date. At the top of the capital structure, the first lien term loan has a coupon of LIBOR + 175 basis points and matures in February 2024. Gross leverage through this loan is approximately 2.5x EBITDA based on estimates for 2022.15 With less than 17 months left to maturity, the loan is a good fit for the CrossingBridge Low Duration High Yield Fund. In their most recent earnings call, the company mentioned that they are evaluating the refinancing of this loan. Given that it will become a current liability by the end of 1Q23, a near-term repayment would not be surprising. While we wait for that event, we’re enjoying a floating rate coupon providing a 5.56% yield-to-maturity based on the quarter-end price of 99. If company were to repay the loan one year prior to maturity, the annualized rate of return would be approximately 7.80% from the end of 3Q22 to February 15, 2023.

Icahn Enterprise (IEP) – Icahn Enterprises LP, headed by investor Carl Icahn, is a diversified holding company with interests in investments, energy, automotive, food packaging, real estate, home fashion and pharmaceuticals. The investment segment derives revenues from gains and losses from investment transactions. Other operating segments, in most cases, are independently operated businesses obtained through a controlling interest. As of 2Q22, Icahn Enterprises had Indicative Net Asset Value of $6.6 billion, consolidated debt of $7.1 billion and total liquidity, comprised of cash, investment funds and revolving credit availability, of $7.2 billion. Moreover, as of the end of 3Q22, it had an equity market capitalization of $16.0 billion. Thus, we have no concern regarding credit quality. We have traded in and out of the IEP 4.75% senior unsecured bond, due September 2024, since it was issued in February 2020. In 3Q22, amidst the downdraft in the high yield market, we were able to purchase these bonds at a yield to maturity over 8.20%, very attractive for a 2-year note with such strong credit quality. Purchased at a discount, the bond would have an even higher annualized total return were the company to redeem it prior to September 15, 2023 when it becomes a current obligation. We expect to continue adding to this position opportunistically.

Event-Driven and Corporate Actions – Bonds and loans that are expected to be repaid as a result of mergers and acquisitions, efforts to de-leverage and/or the desire to remove constraining debt covenants.

Seaspan (SSW) – Based in Vancouver, B.C., Seaspan is the world’s largest containership lessor with a fleet of 132 vessels comprising 8% of world capacity. The company is the largest asset owned by Atlas Corp (ATCO), an NYSE-listed company with market capitalization of $4.1 billion. In early August 2022, Atlas received a non-binding proposal to take it private via acquisition by Poseidon Acquisition, an entity formed by large shareholders and the Japanese liner giant ONE. Per the terms of the 6.5% senior unsecured bond due February 2024, de-listing of the parent company would trigger the ability of bondholders to put the bond to the issuer at a price of 101. We were comfortable purchasing the bond after the takeover proposal was announced, because, even if the deal did not go through, the company’s debt (although a bit elevated at 7.0x EBITDA), would be well covered by its high value, critical infrastructure assets that support a gross loan-to-value ratio of only 64%.16 Moreover, we also like the fact that the bonds are the company’s nearest debt maturity, due in early 2024, so that, if the acquisition is not completed, there is a likelihood that it will be repaid in February 2023 when it becomes a current liability, further enhancing return. The CrossingBridge Low Duration High Yield Fund purchased the bond in August at a yield-to-maturity of 6.22%, but with the expectation that the annualized total return will be much higher if the acquisition is completed. Late in 3Q22, it was reported that Poseidon had increased its bid, increasing the probability of a deal. We have continued to purchase the bonds opportunistically in 4Q22.

Clear Channel International BV (CCIBV) – Clear Channel International BV is a subsidiary of Clear Channel Outdoor Holdings, Inc., one of the largest operators of out-of-home (OOH) advertising displays in Europe and Singapore. The subsidiary is the issuer of the 6.625% first lien bonds due in August 2025. The OOH industry has benefited from the “re-opening” theme as outdoor ad spend had been impacted by COVID-19 lockdowns, although Clear Channel International revenues have only recently returned to pre-pandemic levels given longer lockdowns and greater exposure to metro ridership outside of the United States. Short-term contracts provide frequent opportunities to reprice supply in response to inflationary pressures with the added benefit of operating leverage given a high fixed cost base. Clear Channel International generates normalized low- to mid-teens EBITDA margins with high free cash flow conversion. The company's liquidity profile and long-dated capital structure should allow it to withstand a cyclical downturn. We also appreciate the fact that these bonds are the next maturity in the structure, are secured by a first lien on certain U.K. and Nordic subsidiaries and are structurally senior to the company’s holding company debt. With respect to potential corporate actions, management has announced their intention to sell Clear Channel’s European business with proceeds allocated towards de-leveraging. This would also be a likely precursor to conversion of parent company Clear Channel Outdoor to a REIT as these assets do not qualify for the preferential tax treatment of that structure. Thus, if the European assets are sold, it likely would result in early retirement of the bonds as the restricted payments covenants prevents the company from up-streaming asset sale proceeds to de-lever the holding company. In 3Q22, the CrossingBridge Low Duration High Yield Fund and the CrossingBridge Responsible Credit Fund purchased Clear Channel International’s secured bonds at a weighted average yield-to-maturity of 8.94%. With the bonds callable at 101.65 beginning in on February 1, 2023 and trading at approximately 93 as of the end of 3Q22, there is potential for a much higher rate of return if the bonds are called early.

Potential Takeover Targets – Bonds and loans issued by companies with relatively low leverage and high cash flow that, with the dramatic decline in equity valuations, may make them ripe to be acquired. In such an event, there is an increased likelihood of early repayment or improvement in credit quality.

Fiven AS (FIVENA) – Acquired from Saint-Gobain in 2019 by private equity investor OpenGate Capital, Fiven, is a Norway-based global leader in the production of silicon carbide grains and powders. The materials are used in end markets including construction, engineering, automotive, electronics, aerospace, healthcare, energy, etc. We made our original investment in Fiven’s €70 million secured floating rate notes, due June 2024, paying interest at EurIBOR plus 6.85%, when it was issued in June 2021. Since then we have traded the bonds several times, most recently in 3Q22 when the CrossingBridge Low Duration High Yield Fund and the CrossingBridge Responsible Credit Fund purchased bonds at a weighted average yield of 8.26%. Since the bond was issued, the company has performed very well with 2022 revenues projected to increase by 52% and EBITDA expected to more than double.17 As a result, net leverage has declined from 2.3x to 1.3x since 2Q21. Moreover, as a result of strong performance, cash has been building on the balance sheet, yet, due to restrictive covenants in the bond indenture, the company is prohibited from paying dividends to its shareholders. While we are content to hold the bond to maturity given its yield and credit quality, we suspect the private equity sponsor may take steps to prepay the bond as early as the first call date in December 2022 as part of a dividend recap in which it will take out a significant dividend.

G-III Apparel Group (GIII) - G-III Apparel is a global designer, manufacturer and distributor of branded apparel. Owned brands include DKNY and Karl Lagerfeld; licensed brands are headed by Calvin Klein and Tommy Hilfiger. While top line revenue and gross profit margins have largely returned to pre-pandemic levels, the company’s public valuation has traded down to historical lows (~4.4x P/E, 3.8x EV/EBITDA) ahead of recession worries. At these depressed valuations and given low leverage and steady free cash flow generation, we see G-III as a potential target for strategic or private equity acquisition. In 3Q22, we began establishing a position in G-III’s 7.875% secured bond maturing in 2025, buying at price of 91 for a yield-to-maturity of 11.65%. With gross leverage of 1.3x EBITDA, we are confident in the credit and would be content to hold to maturity. In the event the company is acquired, however, the change of control put at 101% of par would likely accelerate repayment. Likewise, a sale of significant assets might lead to redemption of a portion of or all of the bonds at a price of 100. Thus, we view this investment as an attractive bond with a “call option” for a higher total return if there is an M&A event.

Picking our spots, rolling with the punches, and patiently awaiting the time to come out swinging,

David K. Sherman and the CrossingBridge Team

Endnotes:

1 “Rope-a-Dope” is a boxing technique in which a fighter leans against the ropes of the boxing ring in a defensive position, allowing his opponent to make non-injuring blows while he looks for opportunities to go on the offensive. Eventually, when the opponent is worn out, the boxer can go on the attack to devastating effect. This strategy is most famously associated with Muhammad Ali in his October 1974 match, staged in Zaire, Africa and dubbed the “Rumble in the Jungle”, against world heavyweight champion George Foreman. https://www.youtube.com/watch?v=nCOvjkbEn3c

2 All Star Charts, allstarcharts.com

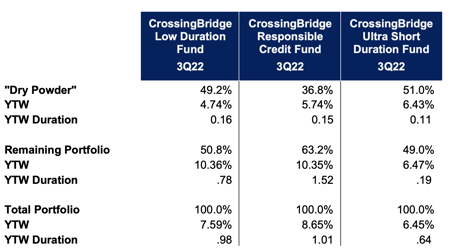

3 “Dry powder”, in the context of our portfolios, is defined as cash and investments that are expected to be repaid within 90 days as a result of call, redemption or maturity as well as pre-merger special purpose acquisition corporations (SPACs). The table below reflects dry powder for each CrossingBridge fund as of the end of 3Q22.

4 “Money good” is a term used by CrossingBridge to describe debt it believes will be paid off in full under current market conditions and on a strict priority basis.

5 FRED Economic Data, Federal Reserve Bank of St. Louis https://fred.stlouisfed.org/

6 These tensions were discussed in our 1Q22 letter, Locomotive Breath, and our 2Q22 letter, In Flanders Fields.

7 ICE BofA US High Yield Index, ICE BofA 10-Year US Treasury Index. Calculated based on the high yield credit spread, less taxes at a rate of 34%, less 200 basis points of assumed credit losses, divided by the 10-year US Treasury rate.

8 ICE BofA US High Yield Index

9 The graph above uses the high yield spread calculated by subtracting the 10-year Treasury rate from the yield-to-worst of the ICE BofA US High Yield Index. This differs from the index spread to worst, however, which is the index yield-to-worst less the corresponding Treasury rate which varies daily. Actual credit spread data for periods prior to the end of 1996 is limited.

10 A punch thrown with full force and commitment that can be a knockout blow if landed.

11 See our 2Q19 investor letter, Rise of the Living Dead, for a discussion of “zombie companies”.

12 Bank of America Global Research

13 ICE BofA US High Yield Index, S&P/LSTA U.S. Leveraged Loan Select Equal Par Value Index

14 The call premium based on “treasury make-whole” call protection is calculated by discounting all of the scheduled principal and interest payments of the bond by the Treasury rate (plus, typically, 50 or 75 basis points) that corresponds to the bond’s maturity. This premium may not be less than 0 so, if rates rise such that the premium would be negative, the call price is par.

15 Bloomberg, sell-side analyst estimates

16 DNB 10/13/22

17 Crushing expectations, bond looks cheap at 750 bps (Fiven), Pareto Securities, August 29, 2022