![]()

Zombies! Coming to a fixed income portfolio near you! They eat your capital to survive!

“Zombie companies”[1] were defined in a recent Bank for International Settlements (“BIS”) study[2] as non-financial companies that are over 10 years old and that are unable to cover their interest expense from current operating income for three consecutive years.

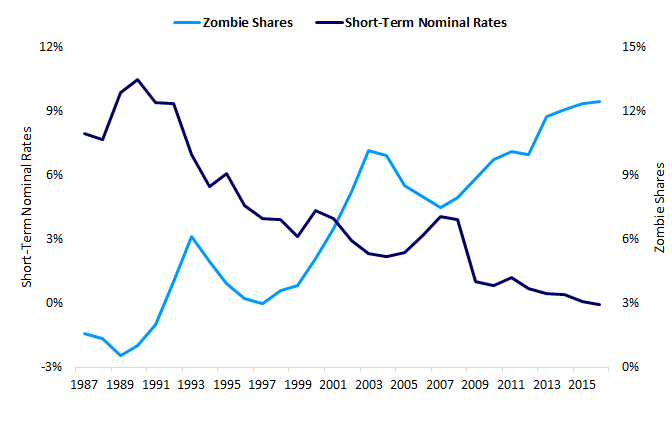

Declining Interest Rates Drive an Increase in Zombies[3]

As shown above, the BIS study of 32,000 companies in 14 developed countries[4] shows that the portion of zombie companies has been rising, with some variability tied to economic cycles, from the late 1980s through 2016. While zombies accounted for approximately 12% of the companies in the study, another BIS report[5] estimates that, as of the end of 2015, over 16% of US companies should be considered zombies. The study also revealed a strong correlation between the rise in the number of zombies and the decline in short-term interest rates. We believe this is due, in part, to the loosening of lending standards by yield-hungry lenders and investors that have been willing to “kick the can down the road” for increasingly risky companies with deteriorating business models. Seemingly, investors have bought into the notion that leverage ratios[6] are less relevant than interest coverage[7]. We beg to differ. Taken to an absurd extreme, investors might permit a company to have an ever-increasing amount of debt as interest rates decline toward zero. Unless such a company takes advantage of cash flow in excess of interest expense to build reserves or de-lever, a day of reckoning can only be postponed for so long with the potential for more dire consequences for creditors.

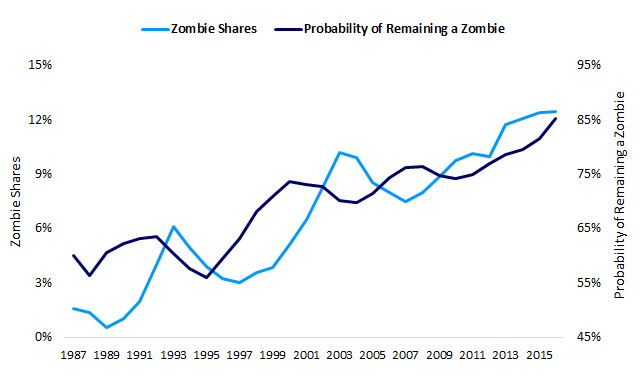

Zombie Firms are Surviving Longer[8]

Research has also shown that the statement “once a zombie, always a zombie” has some merit as the probability of zombie companies failing to improve despite a transfusion of new capital has been increasing since the late 1980s.[9] Further, the deterioration in lender protections, in the form of less restrictive covenants, allows weak companies to raise additional debt and continue operating in situations that in the past would have led to defaults, thus further facilitating the rise of zombie companies. Further, deterioration in lender protections[10], in the form of covenants, over the last several years has also facilitated the rise in the number of zombies.

Given all this, we were curious as to the portion of the U.S. corporate bond market that might be considered zombies for the period 2016-18. We use as proxies iShares iBoxx Investment Grade Corporate Bond ETF (“LQD”)[11] and the iShares iBoxx High Yield Corporate Bond ETF (“HYG”)[12]. In both cases, we eliminated issuers that did not publicly provide financial data and financial companies (e.g. banks and financial services providers). We also modified the definition of a zombie to include those companies with interest expense coverage of less than 1.0x using EBITDA[13] less capital expenditures to represent cash flow.

(EBITDA-Capital Expenditures) / Interest Expenses Less than 1.0x (2016-2018)[14]

| Total Included | Zombies | % Zombies | |

| LQD | 244 | 24 | 9.80% |

| HYG | 241 | 46 | 19.10% |

Similar to the findings of the BIS studies, zombie companies accounted for 19.1% of the high-yield issuers included in our analysis of the HYG and nearly 10% of the investment grade. The majority of investment grade zombie companies were rated BBB, potentially on the cusp of a downgrade to high yield.[15] High yield zombie companies were nearly evenly distributed among BB, B and CCC ratings categories. It is worth noting that our decision to measure interest coverage after capital spending may have identified a small number of companies as zombies which, during the subject time period, were in the midst of multi-year investment programs, the funding of which significantly reduced interest coverage. At times, a company may risk temporary credit quality impairment by embarking on a large capital investment program with the expectation of improved profitability or enhanced shareholder value. That said, a capital program that causes interest coverage to fall below 1.0x for three successive years is likely to be significant and should the execution not meet expectations, the company’s credit health may be permanently impaired.

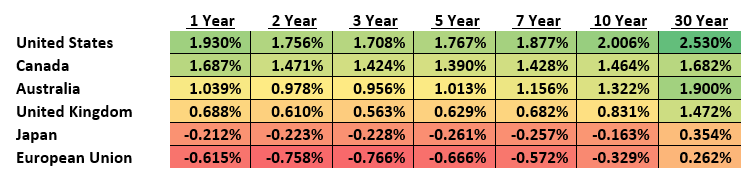

Worldwide Yield Curves - June 28, 2019[16]

As shown above, interest rates around the world are very low. Notably, as of June 28, 2019, interest rates for bonds issued by Japan and members of the European Union, representing 28% of 2018 global gross domestic product, were negative for all maturities out to 10 years.[17] These low rates create a perverse incentive for risky capital allocation. Capital investments and new ventures that were deemed too risky and may not have been funded in a higher rate environment become more attractive when the cost of money is much lower. This can result in challenges for established firms that must now compete with companies’ intent on disrupting the status quo. Thus, in evaluating the future profitability and continuity of established business models, investors must consider the competitive threat of well-funded peers and upstarts. For example, Tesla[18] has been allowed easy access to the capital markets to launch revolutionary (green) cars[19] and potentially disrupt the global automobile industry.

The proliferation of “unicorn”[20] initial public offerings (“IPOs”) in the equity market is also reflective of investors’ willingness to take on greater risk. A big payday is even more attractive when opportunity costs[21] are very low. Over the last five years, 54 unicorn companies have gone public and are currently listed but were not profitable at the time of their IPO and remain unprofitable today. Of these, the top ten, in terms of market capitalization, are likely familiar names:

Last 5 Years - Never Profitable IPOs [22]

| Company | Market Cap (6/28/19) | Description |

| Uber Technologies | 78,640 | Ride hailing services |

| Snap Inc | 19,163 | Technology and social media services |

| Lyft Inc | 19,096 | Ride hailing services |

| Sea Ltd | 14,782 | Information technology services |

| Pinterest Inc | 14,768 | Operates and maintains social networking site |

| Chewy Inc | 14,195 | Online retailer of pet products |

| VICI Properties Inc | 10,161 | Owner, acquirer, and developer of real estate |

| Beyond Meat Inc | 9,661 | Develops plant-based protein food products |

| MongoDB Inc | 8,415 | Develops database software |

| Guardant Health Inc | 7,880 | Biotechnology company |

| TOTAL: | 196,761 |

As they say, “forewarned is forearmed.” AMC Network’s series, “The Walking Dead,” makes it abundantly clear that one better have a knife or gun to fend off zombies. Although the best way to deal with zombies is usually to avoid getting involved in the first place, the experienced high yield investor, as shown in the examples of recent investments below, may also find ways to make zombies work for them, providing attractive rates of return even while the company staggers on.

Weatherford International Ltd. (“WFT”)[23] - Weatherford International is a leading multi-national oilfield services company based in Houston. Since the precipitous decline in oil prices in 2015, the company has been unable to generate EBITDA sufficient to cover its annual capital expenditures and interest expense despite a rise in oil prices since that time. Thus, Weatherford had become a zombie, overburdened by interest expense and unlikely to see a return to the boom years when it could support both a high debt level and operational expansion. In May of this year, Weatherford indicated its intention to file a prepackaged bankruptcy through which it intended to restructure its $7.5 billion of debt to more appropriate levels. While the company had not yet specified whether its term loan would be refinanced with a debtor-in-possession (“DIP”) loan or stay outstanding through the bankruptcy, we were comfortable investing in the $310 million 1st lien senior secured loan, with leverage through that level of less than 1.0x EBITDA and solid collateral coverage. The CrossingBridge Low Duration High Yield Fund purchased the Weatherford term loan in mid-to-late May at prices slightly below par, yield to expected maturity in the mid-single digit rate-of-return on a short term holding. With proceeds from a DIP financing, the company repaid the loan at par, with all accrued interest, after the Chapter 11 filing in early July.

Eastman Kodak (“KODK”)[24] - Eastman Kodak exited bankruptcy in 2013. The company’s post-restructuring strategy was to monetize its patent portfolio, exit mature businesses and develop its growth businesses such as digital imaging and flexographic printing. However, sales of assets and intellectual property fell short of expectations and development of new products took longer than expected. Thus, with EBITDA after capital spending barely covering interest expense in 2016 and falling short since then, Kodak was showing signs of becoming a zombie by mid-2018. Nonetheless, with confidence in the value of its intellectual property, offshore cash holdings and several businesses with positive prospects, we had become comfortable with both CrossingBridge funds holding the company’s 1st Lien Loan, due 2019. In August 2018, however, with the loan’s maturity fast approaching, the company announced its intention to sell the flexographic printing business to pay off most of its debt, expecting to refinance what remained thereafter. In November 2018, the company announced a sale agreement after which we opportunistically added to our position in both funds. Kodak closed the sale in early April 2019, paying off 79% of the loan with the proceeds. Anticipating a near-term repayment of the balance of the loan via new financing or additional asset sales, we added to our position in the remaining “stub” loan, purchasing it at a discount to par following the initial repayment. The remainder of the loan was repaid in late May following issuance of $100 mm of convertible preferred stock. Thus, although Kodak was a zombie, the rationalization of its balance sheet through bankruptcy allowed the company to rise from the dead, post-restructuring, to develop new businesses and build enough enterprise value to enable it to repay its debt.

Attending a horror movie, you may be tempted to cover your eyes when it gets really scary. Credit investors who cover their eyes risk losing their capital in some zombie companies and missing out on profitable opportunities offered by others.

Head on a swivel, on the lookout for zombies,

David Sherman and the CrossingBridge Team

Endnotes

1 During Japan’s “Lost Decade” of the 1990s, banks continued to offer favorable financing to unprofitable borrowers rather than reclassify their loans as nonperforming. The term “zombie companies” was coined to reflect these borrowers. For further discussion of the repercussions of this practice in Japan, please refer to Zombie Lending and Depressed Restructuring in Japan, Caballero, Hishi and Kashyap, American Economic Review, December 2008 https://economics.mit.edu/files/3770.

2 The rise of zombie firms: causes and consequences, Banerjee and Hofmann, Bank for International Settlements (2018) https://www.bis.org/publ/qtrpdf/r_qt1809g.pdf

3 The rise of zombie firms: causes and consequences, Banerjee and Hofmann, Bank for International Settlements (2018) https://www.bis.org/publ/qtrpdf/r_qt1809g.pdf in which the sources are identified as Banerjee and Hofmann (2018); Datastream Worldscope; authors’ calculations.

4 Australia, Belgium, Canada, Denmark, France, Germany, Italy, Japan, the Netherlands, Spain, Sweden, Switzerland, the United Kingdom and the United States

5 BIA Quarterly Review, Bank for International Settlements, September 2017 https://www.bis.org/publ/qtrpdf/r_qt1709.pdf

6 Total net debt divided by annual free cash flow i.e. the total number of years for a company to pay off its debt.

7 Annual free cash flow divided by annual net interest expense i.e. the number of times that free cash flow covers coupon payment. If the number is less than 1.0x, the company would need to find the cash to pay its interest expense by reducing working capital, selling assets or borrowing additional money. Even if the ratio is above 1.0x, the company may still need sources of capital to support its business model.

8 The rise of zombie firms: causes and consequences, Banerjee and Hofmann, Bank for International Settlements (2018) https://www.bis.org/publ/qtrpdf/r_qt1809g.pdf in which the sources are identified as Banerjee and Hofmann (2018); Datastream Worldscope; authors’ calculations.

9 Incidence of a zombie firm remaining a zombie in a fourth consecutive year.

10 Refer to our previous investor letters. Most recently, a brief discussion was provided in the 3Q2018 Shareholder Letter on page 4.

11 As of 3/31/2019 our position in LQD represented 0.00% of the Low Duration Fund and 0.00% of the Long/Short Fund. As of 6/30/2019 our position in LQD represented 0.00% of the Low Duration Fund and 0.00% of the Long/Short Fund.

12 As of 3/31/2019 our position in HYG Options represented 0.0% of the Low Duration Fund and 0.0% of the Long/Short Fund. As of 6/30/2019 our position in HYG Options represented 0.00% of the Low Duration Fund and 0.0% of the Long/Short Fund.

13 Earnings before interest, taxes, depreciation and amortization.

14 Bloomberg, iShares, iShares iBoxx $ Investment Grade Corporate Bond ETF and iShares iBoxx $ High Yield Corporate Bond ETF

15 For more discussion of BBBs, please refer to our 2Q18 Commentary, Float Like a Butterfly, Sting Like a (Triple) B

16 Source: Bloomberg

17 Source: Bloomberg, Wikipedia https://en.wikipedia.org/wiki/List_of_countries_by_GDP_(nominal) and World Economic Outlook Database, April 2019, International Monetary Fund https://www.imf.org/external/pubs/ft/weo/2019/01/weodata/index.aspx

18 As of 3/31/2019 our position in Tesla represented 0.00% of the Low Duration Fund and 0.00% of the Long/Short Fund. As of 6/30/2019 our position in Tesla represented 0.00% of the Low Duration Fund and 0.00% of the Long/Short Fund.

19 Some people will argue that Tesla is more than an auto company, but, rather, it may also be more broadly disruptive to the production and distribution of energy.

20 A unicorn company is a privately-held startup company valued at over $1 billion.

21 Opportunity cost is a loss of potential gain from other alternative investments when another investment is chosen. In the low yield environment, an investor choosing to invest in speculative equities rather than more conservative fixed income instruments is foregoing a low rate of return by choosing not to invest in fixed income.

22 Source: Bloomberg. None of these positions held in either fund in 2Q19.

23 As of 3/31/2019 our position in WFT represented 0.00% of the Low Duration Fund and 0.00% of the Long/Short Fund. As of 6/30/2019 our position in WFT represented 0.55% of the Low Duration Fund and 0.00% of the Long/Short Fund.

24 Previously Kodak was discussed in our 3Q2018 CrossingBridge Low Duration High Yield Commentary on page 6.

As of 3/31/2019 our position in Eastman Kodak represented 1.16% of the Low Duration Fund and 1.83% of the Long/Short Fund. As of 6/30/2019 our position in Eastman Kodak represented 0.00% of the Low Duration Fund and 0.00% of the Long/Short Fund as the position was paid off in May 2019.

Credit Ratings discussed in this piece are from the Bloomberg Composite comprised of ratings from S&P, Moody's, Fitch, and other credit rating agencies.

Definitions: Yield to Expected Maturity is the annual return an investor would receive if he or she held a particular bond until its expected maturity.